- City Fajr Shuruq Duhr Asr Magrib Isha

- Dubai 05:07 06:22 12:05 15:16 17:42 18:57

Photo: File

Dubizzle Property, the UAE’s biggest and most visited property platform, in collaboration with JLL, the world's leading real estate investment and advisory firm, reveals joint Abu Dhabi Property Market Overview report, analyzing the capital’s residential and commercial real estate market.

Findings show a further decline in residential sale and rental prices in Q1 2017 compared to Q1 2016, as well as a decline in commercial and retail property prices, which is expected to continue throughout the year.

Residential sale and rental prices decline following reduction in transaction volumes and sentiment

The joint report revealed that villa projects experienced the steepest year-on-year decline in sales prices.

Golf Garden Villa prices dropped by 11% compared to last year and are now selling at a median sale price of Dh1,005 per sq.ft.

A decline was also recorded for villas in Al Raha Beach (8%), Al Reef (6%), and Al Zeina (4%), while Saadiyat Beach Villas experienced no change compared to last year with the median sale price per sq.ft. pegged at Dh1,524.

Similarly, apartment sale prices decreased with Al Reef Downtown and Al Reem Island apartments dropping by 4% and 7% respectively.

Al Bandar experienced the sharpest decline (21%), followed by Sadiyaat Beach Apartments (7%). Al Ghadeer Village apartments, located on the outskirt on route to Dubai, however, experienced an increase in sale prices by 2%.

The continued reduction in transaction volumes and sentiment in the capital saw property sale prices decline in 2016, which has continued into the first quarter of this year.

“A decline both in the rental and sale segment is further expected in the capital - fragmented in nature, with some communities and property types to be affected more than others. It’s important for developers to observe the property types in demand; Abu Dhabi is known for its family-feel, hence the most searched property types on dubizzle in 2016 for key popular communities showed 2 BR apartments for apartment seekers and 4 and 5 BR for villa seekers both in the rent and sale segment. This is very different to Dubai, where 1 BR apartments in prime communities always taking the lead in search volumes.” commented Ann Boothello, Senior Product Marketing Manager of Property at dubizzle.

Residential rental prices within prime areas continue to decline due to higher vacancy rates due to challenges within certain industries such as petrochemical and financial services sectors in 2016, particularly affecting the higher-end segments and larger residential units.

The report has revealed that rental prices for three-bedroom villas in Al Zeina, Al Raha and Al Reef decreased by 8% to 12% compared to last year. Two-bedroom villas were the most popular search properties in Al Reem Island for rent, which experienced the shallowest dip in price (7%), while one-bedroom apartments declined the most (15%).

“Abu Dhabi witnessed significant supply completions from 2009 to 2014 across all sectors due to major land releases following the launch of the 2030 plan and the creation of large-scale master developments across Abu Dhabi. This led initially to over-supply and increased vacancy rates, followed by market absorption as major government spending plans and improved sentiment fueled demand,” commented David Dudley, Head of Abu Dhabi Office, JLL.

Dubizzle and JLL anticipate a further decline in certain sub-sectors over the short term due to the current decline in demand growth and sentiment, and in some sectors, increased supply.

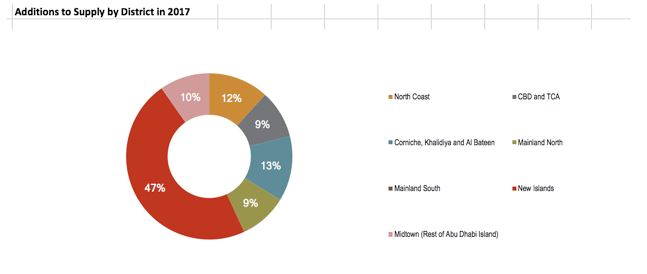

47% of residential supply is expected in New Island Communities in 2017

New Islands districts include Sowwah, Reem Island Districts, Raha District, Al Raha Beach, Saadiyat Island, and Yas Island. Approximately 3,100 residential units were completed in Abu Dhabi last year, mainly within Reem Island, Saraya, Danet and Rawdhat bringing the total property stock to 248,000 units in the capital.

“Since 2015 annual supply completions have dropped to long-term lows as the market adjusted, liquidity tightened, developers became more cautious and due to the impact of tightened planning policy and the new real estate regulations. This reduction in annual supply completions is welcomed at a time of weaker demand. While demand has reduced largely due to the decline in oil prices and the resultant impact on government spending and sentiment, reduced supply completions have mitigated the extent of over-supply" Dudley added.

There are currently around 5,000 units scheduled for completion in 2017, however, dubizzle and JLL anticipate a significant proportion of this is likely to be delayed at the final stages of approvals and handover, further mitigating the negative impact of reduced demand.

Future residential supply is expected to shift to the New Island Communities, particularly Reem Island, Yas Island, Saadiyat Island and Al Raha Beach.

Commercial space rental prices experience drastic drop compared to last year

According to dubizzle data, search volumes for office rental space almost halved (47%) between Q1 2016 and Q1 2017, indicating less demand for commercial property comparing Q1 2016 to Q1 2017.

Commenting on the commercial market, Boothello said: “Demand for office space has remained generally flat during 2016 due to the decline in oil prices directly impacting the oil related sector and indirectly impacting other sectors due to a slowdown in government spending. Average Grade A and Grade B office rents have decreased by 2% and 5% in Q3 2016 reaching approximately Dh1,760 per sqm and Dh1,030 per sqm respectively.”

The rise of high profile mergers such as NBAD and FGB, as well as Mubadala Investment Company and IPIC, have also caused shifts in the capital’s office scene.

In terms of retail space, rental prices have declined by 58% while the sales costs have gone down by a sweeping 84%.

“We expect the market to remain suppressed this year and next, although there are signs of 2017 and 2018 supply completions being higher than 2015-2016.

As market conditions start to improve in Dubai and government spending returns to Abu Dhabi, the market will head back towards recovery and it will be important for supply completions to remain balanced”, concluded Dudley.

![]() Follow Emirates 24|7 on Google News.

Follow Emirates 24|7 on Google News.